“Ahh, the P/E’s ‘inevitable’ (as you would say) reversion to the mean, eh mmb?“

Spot-on steady you are, Squire. Since instituting the honestly-calculated “live” price/earnings ratio of the S&P 500 a decade ago, you clearly can see the P/E (green) always reverts to its evolving average (red). Let’s too be honest about the “E”: thus far in Q2 Earnings Season, some 80% of S&P 500 constituents have reported, their combined capitalization-weighted EPS increase from a year ago being +6%, a respectable gain fairly in line with the rate of inflation (of which the stock market is a hedge). The problem remains that stock prices collectively indexed per the S&P 500 — vis-à-vis earnings — are terrifically expensive, especially given the positive interest rate environment, (such extreme risk variance upon which herein we’ve gone on ad nauseam).

Nevertheless with respect to the above P/E graphic, let’s do the foreboding math (a rarity in financial management these days). The “live” P/E today is 54.9x, varying vastly from your stockbroker parroting that “it’s twenty-something”. The evolving average is 40.3x. Thus to bring the “P” in line with the “E”: the reversion calls for an S&P 500 price “correction” from today’s 4478 down to 3290, (i.e. -27%). As well — rightly or wrongly — we’d written earlier in the year for the S&P perchance to reach sub-3000; or as our initial reader (one J.G.S.) from the inception of The Gold Update quipped away back in 2009: “There’s always the overshoot”. And by the above graphic, indeed there regularly is negative overshoot down through the red line.

Further we again remind: had COVID never occurred such that the money supply had never ballooned, the top of the S&P 500’s 50-year regression channel today would be 2800. Isn’t math wonderful?

As for the usually “rah-rah for ratings” FinMedia, we credit Bloomy with having come ’round to reality a bit, their headlining this past Tuesday that “Stocks pull back from July rally on weak earnings”, albeit we did ask ourselves for the bazillionth time “They’re just figuring this out now?” ‘Tis why we maintain the Earnings Season page at the website, which deep into Q2 results shows 50% of some 1,400 reporting companies having beaten their bottom lines from a year ago … which means 50% have not so done, (just in case you’re scoring at home).

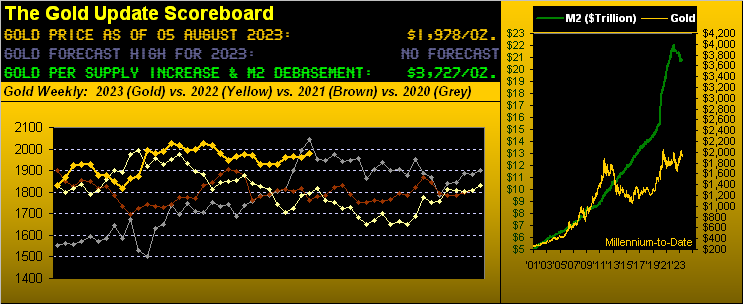

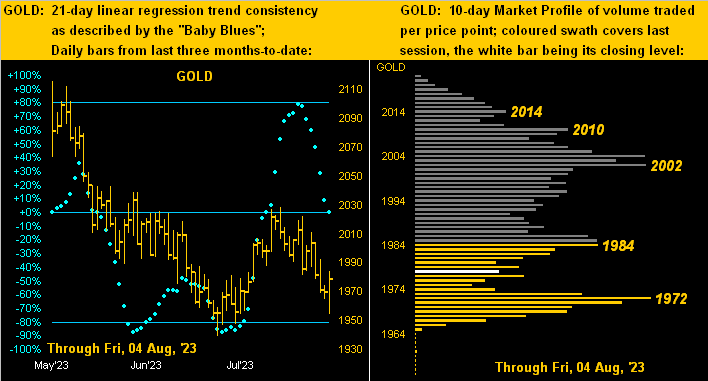

Let’s next move on to assess Gold’s scoring via the following two-panel graphic of the daily bars from three months ago-to-date on the left and 10-day Market Profile on the right. (Note: both panels are fully in December contract pricing; to view the effect of the aforementioned 40-point premium gap, please see the website’s page for either “Gold” or for “Market Trends”). Either way, yesterday Gold was well in play as you can see by its rightmost daily bar, even as the baby blue dots of regression trend consistency continue to descend. As for the Profile, the most dominantly-traded price in December terms for the past fortnight is that 1972 supporter, the overhead resistors as also labeled. And yes, Virginia, by the December contract, Gold in the past two weeks has traded to as high as 2022, just 67 points below the 2089 All-Time High from basically three years ago to the day (07 August 2020):