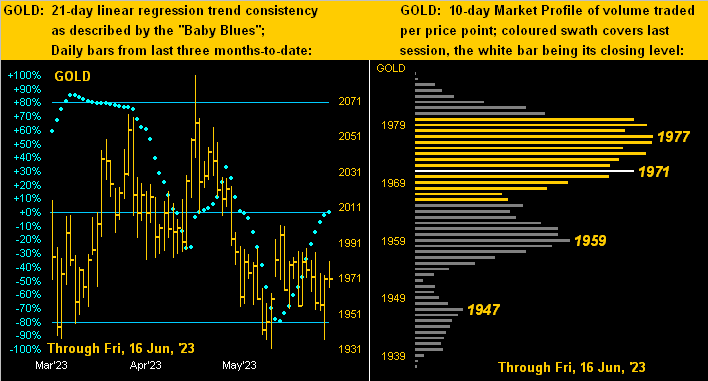

Next let’s go more to The Now with Gold’s two-panel graphic featuring the daily bars from three months ago-to-date on the left and 10-day Market Profile on the right. And with respect to Gold’s “Baby Blues” of regression trend consistency, they’ve recovered up to their 0% axis meaning that price across the past 21 trading days (i.e. one month) has essentially been trendless. That fits well in thus describing Gold as doing donuts, indeed to reprise one of our favourite musical analogies ![]() “Goin’ Nowhere”

“Goin’ Nowhere”![]() –[Chris Isaac, ’95]. As to the Profile, price at present is up against more trading resistance than underlying buoyancy:

–[Chris Isaac, ’95]. As to the Profile, price at present is up against more trading resistance than underlying buoyancy:

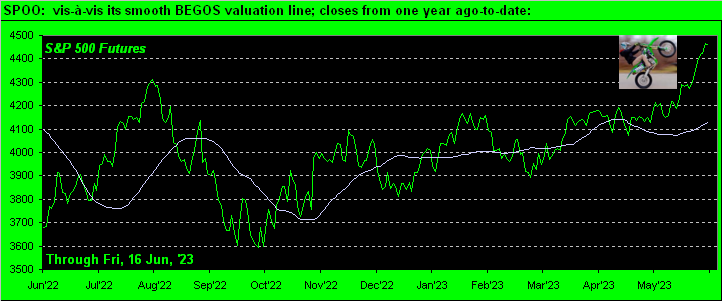

The last time we had such an extreme deviation? ‘Tis right there in August of a year ago. And quick as a wit, the S&P plummeted in mere weeks from 4300 to 3600 (-16%) by September’s end.

But wait, there’s more: upon our “live” p/e of the S&P reverting to its mean (as historically has always happened) given there being hardly any growth in real earnings (“What are those?”), that mathematically calls for S&P 3300 (or -25% from here). But that’s just to the “live” mean, (which has evolved by the day since 2013). For then comes the overshoot, et voilà, we see S&P sub-3000 (or at least -32% from here) as we’ve already on occasion mentioned this year. ‘Course — again historically — the market always comes all the way back. It merely depends on how many years or in some cases decades you’re willing to wait.

Still, we can end on a high note: “BUY GOLD!“ Especially given its being priced today (1971) at just 54% of its true debasement valuation (3658)!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter: @deMeadvillePro