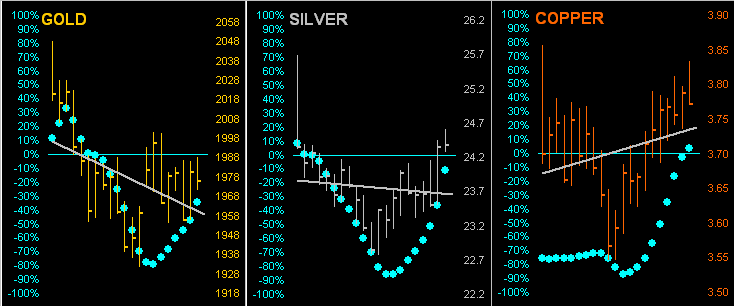

So toward this week’s wrap, let’s assess…

The Gold Stack

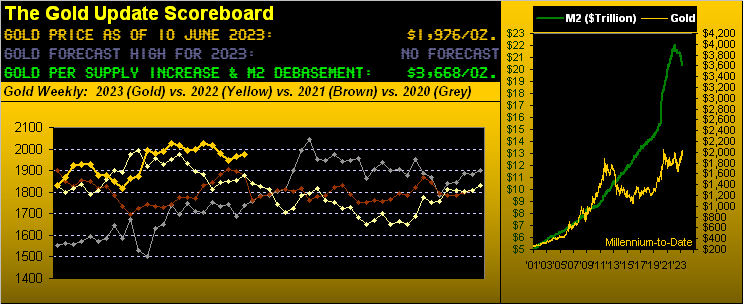

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3668

Gold’s All-Time Intra-Day High: 2089 (07 August 2020)

2023’s High: 2085 (04 May)

Gold’s All-Time Closing High: 2075 (06 August 2020)

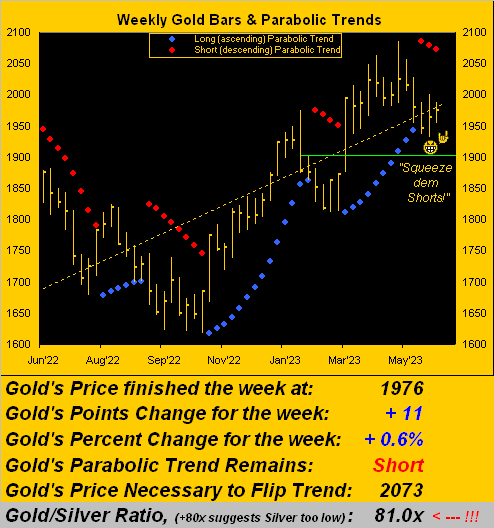

The Weekly Parabolic Price to flip Long: 2073

10-Session directional range: up to 2001 (from 1950) = +51 points or +2.6%

Trading Resistance: 1977 / 1980 / 1991 / 1996

Gold Currently: 1976, (expected daily trading range [“EDTR”]: 26 points)

10-Session “volume-weighted” average price magnet: right here at 1976

Trading Support: 1961

The Gateway to 2000: 1900+

The 300-Day Moving Average: 1841 and rising

2023’s Low: 1811 (28 February)

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

And indeed to wrap, we couldn’t help but notice this claptrap, courtesy of the UPI, (such as to have former President and Chairman Hugh Baillie likely rolling in his grave): Ready? “Heat-trapping carbon dioxide hit record levels in May … not seen in 4 million years” Really? Moreover, how can it be a record if it already was the case 4 million years ago… Right? We’d really like some clairification on this if any of you valued readers might ring up one of your australopithecus relatives … you know … to find out at what laboratory in what state or country such measurement was made back then, and so forth. Just curious.

‘Course, 4 million years ago is peanuts when we consider that Gold (so ’tis said) extends back some 4 billion years when The World was then being pelted by asteroids. Now that’s real climate change! In fact: “Miss Gibbs? Would you kindly contact Hollywood Studio Rentals and see if we can get H.G. Wells’ time machine for a week or so?” (She’s a winner). Oh to linearly regress the value of Gold from then through now and into the future, WOW!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter: @deMeadvillePro