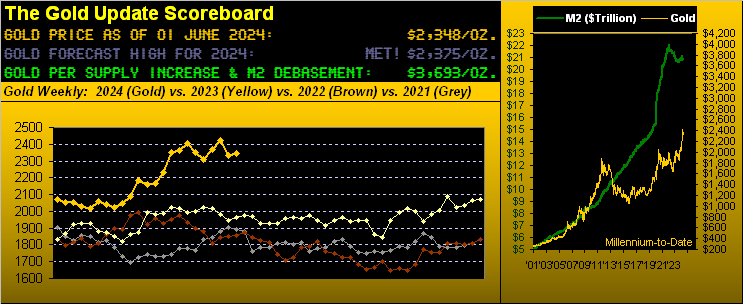

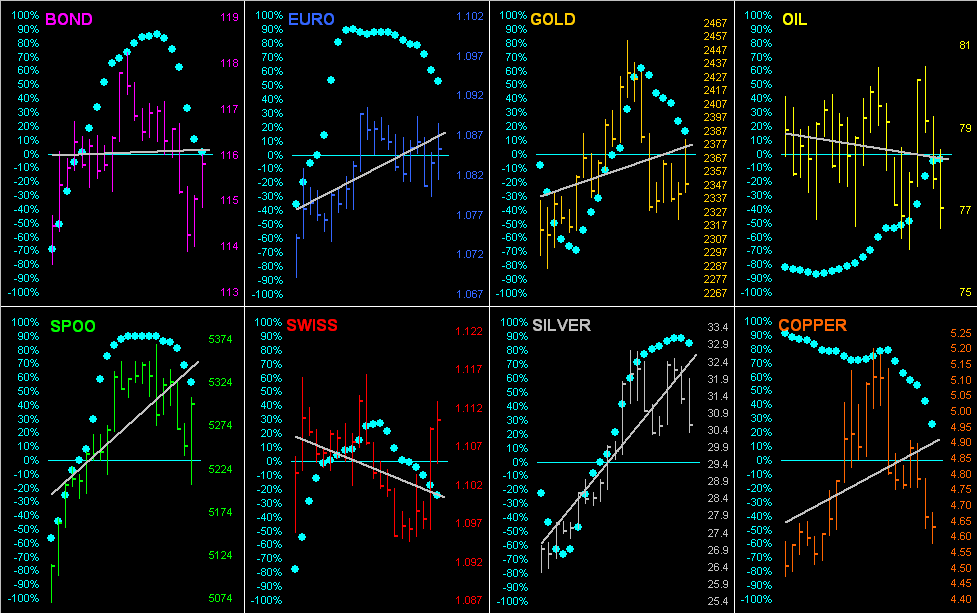

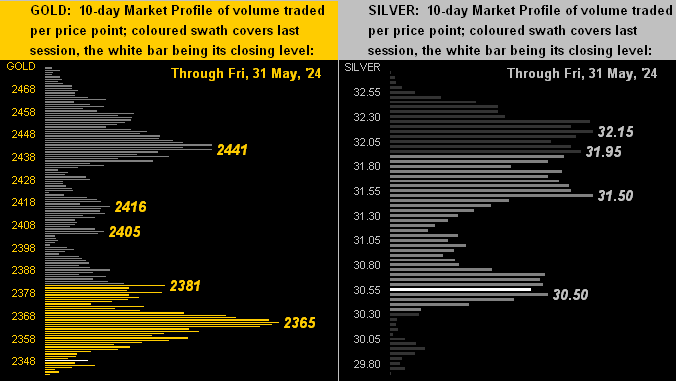

The above chart tracks Gold by its 12-hour bars from nearly the beginning of this year-to-date. (The inset at lower right is by Gold’s daily candles specific to the August contract for the past two months). And stark thereon is the double-top (both being chronological All-Time Highs) achieved at 2449 on 12 April and again at 2454 on 20 May. The rationale for displaying the double-top per 12-hour bars is — that by price’s 12-hour MACD (moving average convergence divergence) — such study presently ranks as Gold’s best Market Rhythm for taking signals followed by profit. Green bars indicate price when the MACD is Long and red bars when Short, the latter as you know being a bad idea; (profitability results of this study are included on the website’s current Market Rhythms list).

The key point of course is that double-tops in major markets are prime for selling (be it by humans or algorithms), which — in spite of our being broad-based bullish on Gold — has been our near-term bearish analytical slant given the abrupt downtrend from that 20 May All-Time High at 2454. Indeed since then, Gold has dropped (basis the June contract) from 2454 to as low as 2321 (-133 points or -5.4% in just eight trading days). Now by the August contract having settled yesterday (Friday) at 2348, should 2309 go, the 21 March high of 2263 ought come into play … just in case you’re scoring at home.

More importantly, what’s coming into play in the words of Bloomy last Wednesday is “Revived Hike Chatter”. For some irrational reason, the FinWorld just seems to be figuring that out now. However, we’ve regularly herein been musing since the start of this year about the Federal Reserve ~~perhaps~~ having to raise rather than cut interest rates. The difference between ![]() “Us and Them”

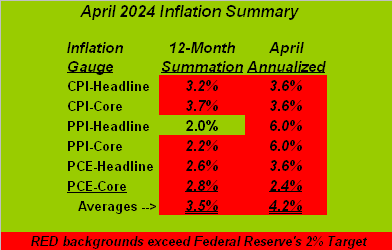

“Us and Them”![]() –[Pink Floyd, ’73] is simple: we do the math; the FinWorld parrot one another. And by the math, inflation remains on the move as below summarized in our April table:

–[Pink Floyd, ’73] is simple: we do the math; the FinWorld parrot one another. And by the math, inflation remains on the move as below summarized in our April table:

Therein are the three major measures of StateSide inflation: the Consumer Price Index (CPI), Producer Price Index (PPI) and “Fed-favoured” Personal Consumption Expenditures Price Index (PCE), all listed with both their headline and attendant core readings. The left column is each category’s 12-month summation and the right column is April’s data annualized. Now look at the two averages, bearing in mind the Fed’s inflation target is 2%: for the 12-month summation ’tis 3.5%; but for April’s annualized paces ’tis 4.2%. Which for you WestPalmBeachers down there means: “We’re going the wrong way…”

So is the StateSide economy. Recall our penning a week ago: “…the Baro looks to be lower still in a week’s time as stagflation creeps ‘cross the nation…” Cue Tag Team from back in ’93: ![]() “Whoomp! (There It Is)””

“Whoomp! (There It Is)””![]()

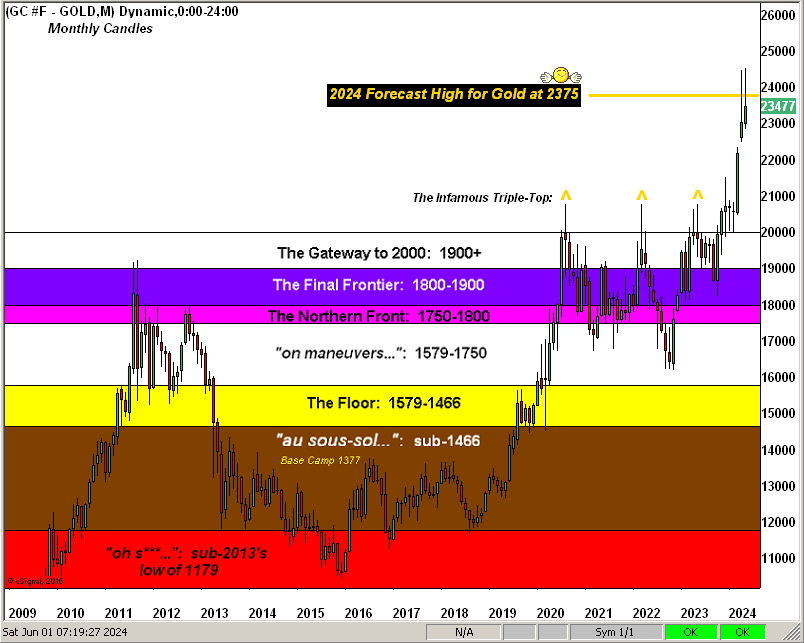

To wrap: with each passing week, more and more internet information (or “bilge” if you will) builds toward financial end-times, part and parcel of which would include our “Look Ma, no money!” S&P crash. ‘Course this being big election years coinciding both on this side of the Pond (five-year Parliamentary) and StateSide (four-year Presidential), the hype of “Well, it’s the election, you know…” already is quite rife. But even were it not, the following macro-prudential fact remains: the S&P 500 is priced at nearly double its earnings support, whilst Gold is priced at nearly half its Dollar debasement valuation. And as we’ve demonstrated ad nauseum throughout 16 years of these weekly missives, price inevitably reverts to valuation. Therefore, near-term price plop or not: hopefully your Gold is well-guarded when sought!

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro