We really like what we’re now seeing for Gold. After many-a-week of downside drudgery, ‘twould appear the yellow-metal is at least poised to make a turn back up, perhaps substantively so. More on that in a minute, but first:

StateSide — it being “The Fourth of July” (No. 250) — let’s start with some feuding fireworks from the FinMedia as regards FedHead Kevin “The Warrior” Warsh this past Thursday at 2026’s European Central Bank Forum in Sintra, Portugal. Both these headlines appeared simultaneously “above the fold” late Thursday by the cited sources:

- Bloomy: “Signs of economic strength alongside easing price pressures … Federal Reserve Chair Kevin Warsh saying inflation risks have come down.”

- CNBS: “Fed Chief Kevin Warsh … says inflation ‘too high'”

Query:

So which is it?

- Have inflation risks actually come down, indicative of no rate hike on 29 July?

- Or is inflation actually too high, supportive of a rate hike on 29 July?

Response:

We already know by simple grade-school arithmetic it ought be the latter. As our May Inflation Summary (herein posted a week ago) showed — and bearing in mind the Federal Reserve’s targeted +2.0% pace — annualized inflation by May’s 12-month average is running at +4.3%, and by annualizing May alone ’tis +5.8%. What ever happened to +2.0%? Warsh wants it. Thus, the second of those queries clearly is the more appropriate … save that today’s mathematically-challenged FinWorld consensus expects the 29 July Open Market Committee voting to “Not raise!”

“But hang on, mmb, ’cause April’s annualized average was +8.0%, so by that, risks are coming down…”

Squire, any way ’tis couched, every major inflation measure is running well beyond the adamantly Fed-targeted +2.0%. That stated, perhaps +2.0% has become archaic. Just as has an S&P 500 price/earnings ratio (now 46.2x) ever returning to the portfolio theory standard of 15x become archaic, (until ’tisn’t).

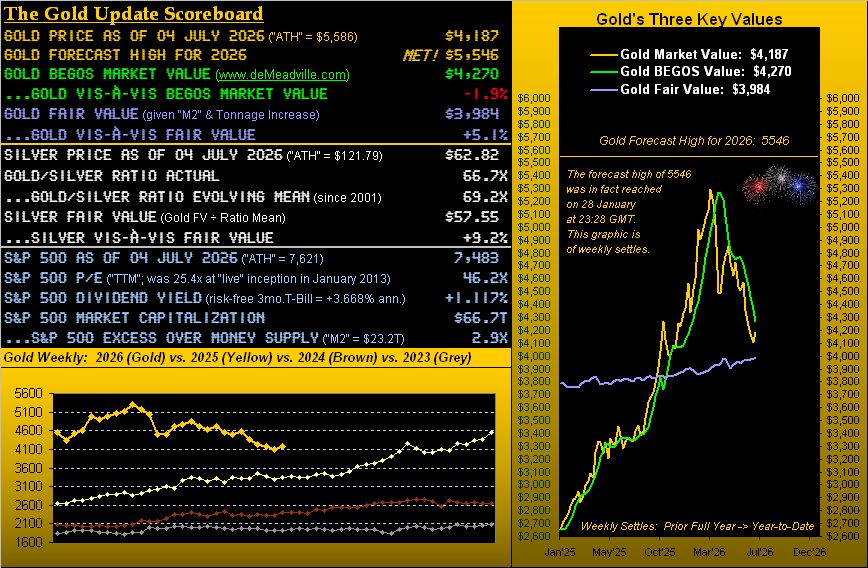

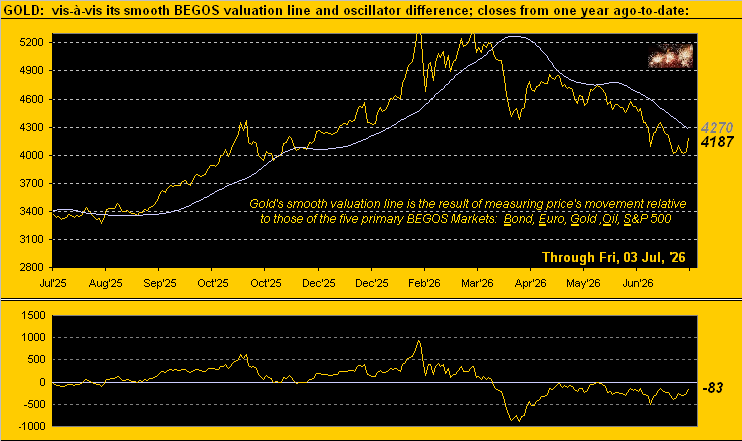

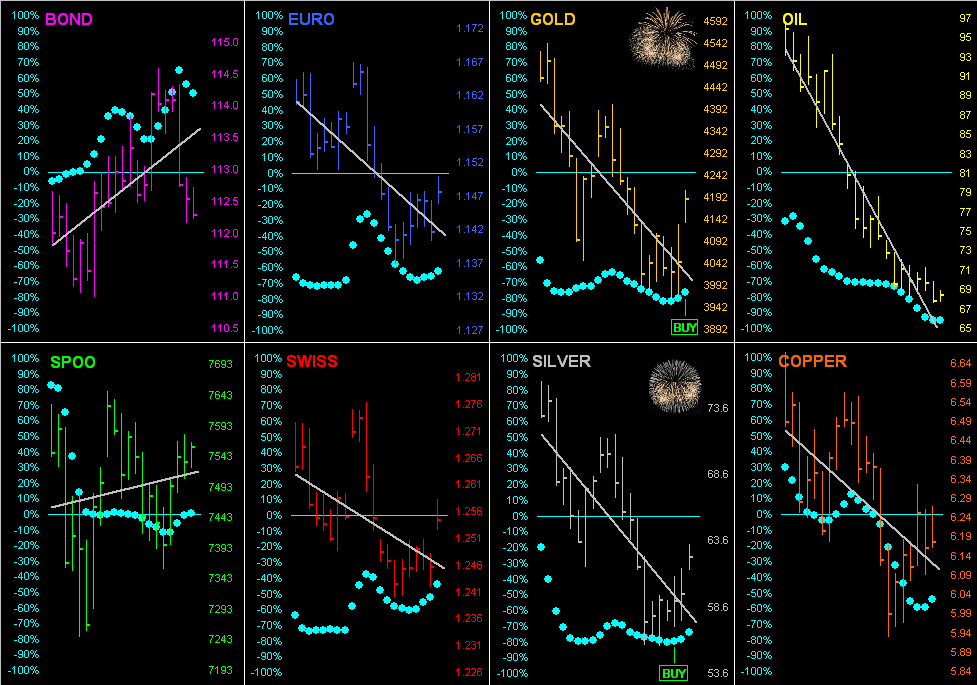

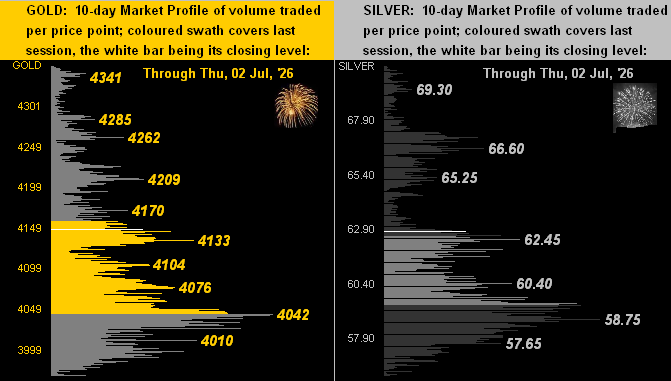

Specific to Gold, its prior-week teasing of Fair Value (now 3984 per the opening Scoreboard) heralded buying. Before Gold’s gain of this past week, 12 of the previous 18 were net down. But price then settled Thursday at 4136 (this holiday-shortened week’s official COMEX close) and yesterday (Friday ) furthered itself to as high as 4208 prior to hitting the abbreviated session’s “trading halt” at 4187 toward Monday settlement, (yes the same unusual scheduling as was the case two weeks ago).

So in turning to Gold’s weekly bars and parabolic trends since this time a year ago, we’ve printed the Friday “halt” price rather than Thursday’s settle, (as technically we’re already trading Monday). Moreover, our sense is Gold — at long last — looks to make an up-run toward, in due course, meeting the cascading red dots of the now 16-week parabolic Short trend. And just in case you’re scoring at home, the midpoint between price (4187) and parabolic (4765) is 4476, i.e. some +289 points above here. Gold’s expected weekly trading range? 269 points. So barring Gold going straight up, ’tis still feasible that this parabolic Short trend shall meet its end come month-end: