‘Tis the Northern Hemisphere’s final day of spring: a season of Gold price reclusion and overall markets’ confusion, further festooned with Fed follies, war worries, and ever-sustained super-inflated S&P 500 insanities.

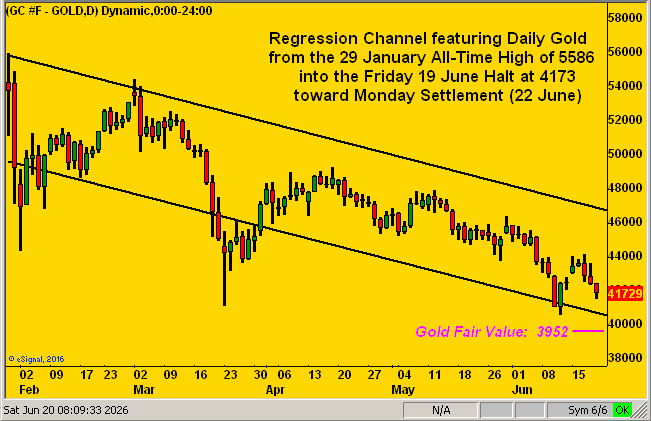

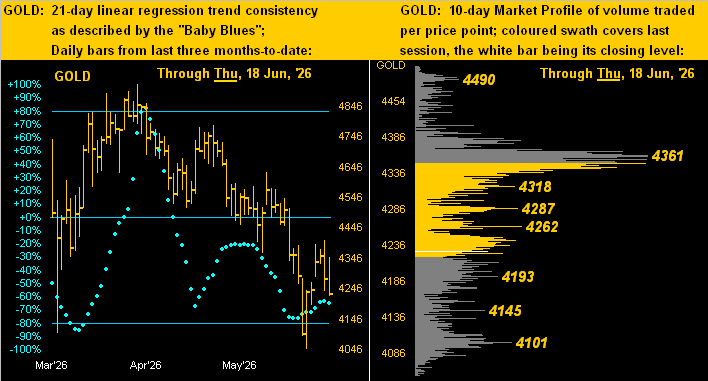

Since Gold opened the first day of spring (20 March) at 4654, price has lost as much as -13.1% to 4046 (just back on 11 June) toward settling this past holiday-shortened week “officially” on Thursday at 4228 — or if you prefer — per yesterday’s (Friday’s) “trading halt” at 4173 toward settlement come Monday: that’s right, this is a Saturday with COMEX Gold “halted” rather than “settled”. When was the last weekend day that happened? Cue San Francisco’s own Jake Holmes’ ![]() “Dazed and Confused”

“Dazed and Confused”![]() –[’67]

–[’67]

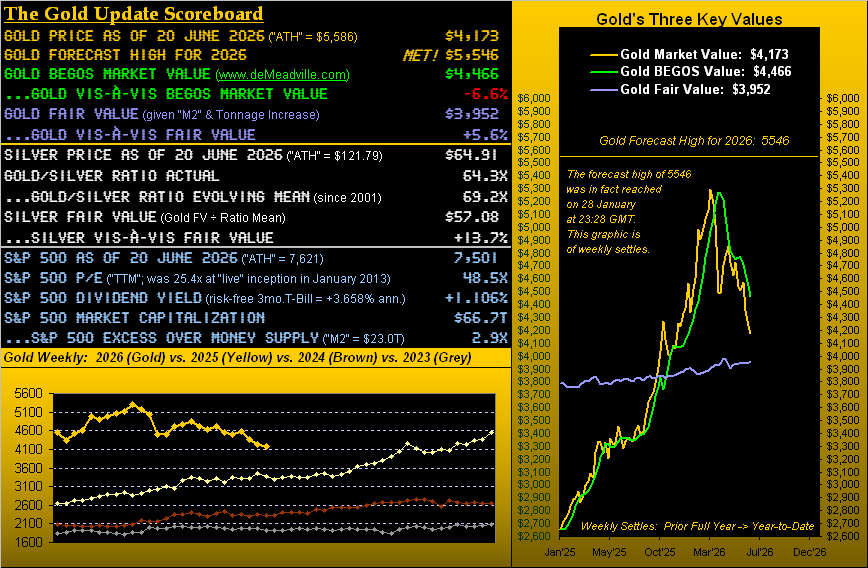

By either “halted” or “settled” price, after having peaked year-to-date at 5586 on 29 January, Gold has been in reclusive withdrawal throughout, today’s 4173 level a net decrease from that All-Time High by -25.3%, price all-in thus far for 2026 being -3.7% (having settled out last year at 4332). Here ’tis by the day through the current 4173 “halt” toward Monday’s settle. Note at the graphic’s lower right (per last week’s musical query “? ♫ Return to Fair Value ♫ ?”) price seemingly on approach to such 3952 level :

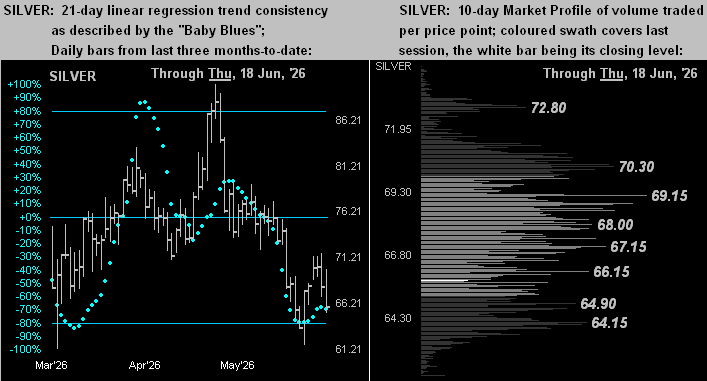

To close, we’ve this from “The Good News Dept.” Century-to-date, “yield-less” Gold now at 4173 is +1,424% and Silver at 64.91 +1,299%. By comparison, the (albeit very scant) yielding “Casino 500” today at 7501 is +631% (or +468% ex-dividends).

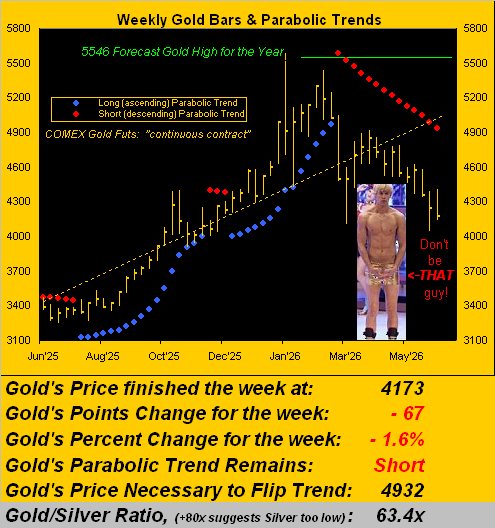

To be sure, the precious metals remain in near-to-medium term downtrends. In fact, this past week the children’s writing pool over at the once-mighty Barron’s just figured it out (and we quote): “[Gold] is dangerously close to bear market territory.” (One wonders where’ve they’ve been since February).

Regardless, when FedHead Kevin “The Warrior” Warsh — dare we say “inevitably” — is called upon to bail out Bessent’s Treasury, look for Gold’s reclusiveness to morph into nothing short (no pun intended) of upside monstrousness.

Still — all that said — are you confused by that within your war chest? What say you, Bunky?

“And I sold my Gold for these??” Bummer.

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro