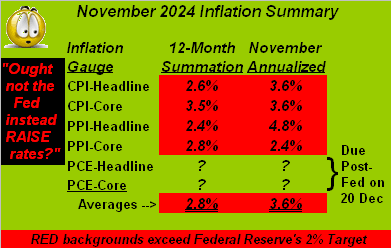

Obviously to complete the above table, we await November’s “Fed-favoured” Personal Consumption Expenditures Prices Index due next Friday, 20 December, which conveniently for the central bank is two days after its Open Market Committee’s 18 December Policy Statement. Regardless, what does our table thus far depict?

At its foot we see the average 12-month summation of the elements is +2.8%; through October ’twas +2.6%… Whoops! Moreover, the November annualized average is +3.6%; that for October was +3.0%… Whoops! Time to pick up the telephone and call the Fed: “Hey Jay! We’re goin’ the wrong way!”

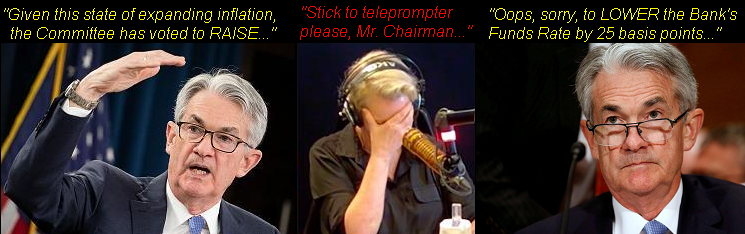

And yet, they’ll likely lop another 25bps off the Funds Rate come Wednesday, as absent of math, the modern-day Fed apparently acts on optics. “A cut is expected? A cut we shall do!” And given rate cuts effectively increase the money supply through the Fed window, more Dollars distributed into the monetary system (barring economic efficiency) lead to more inflation. For more are worth less; the “wrong way”, indeed.

However, to read the also math-challenged FinMedia, increasing inflation is not their take. Hat-tip Bloomy, which in response to rising retail inflation (the Consumer Price Index) ran on Wednesday with “Stocks Rise After CPI Gives Fed Green Light to Cut”. Really? The CPI quickened its October pace of +0.2% to +0.3% for November … which annualized as noted is +3.6% … which further distances itself from the Fed’s +2.0% target. That’s a green light to cut?

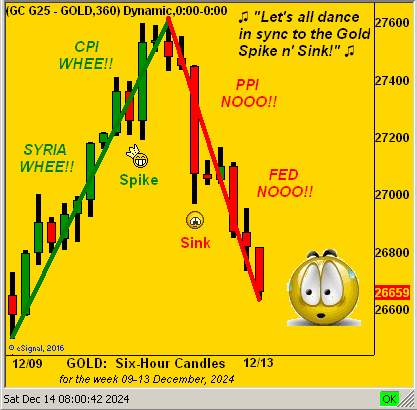

But wait, there’s more: into Wednesday evening Bloomy embellished its response by adding “US Inflation in Line With Forecasts Solidifies Bets on Fed Cuts”. Really? We can only guess that — again mathematics aside — merely meeting forecasts is all that counts, even as inflation increases. This is adroitly akin to contemporary stock market valuation: the substance of earnings (or lack thereof) no longer has meaning, just as long as they “beat estimates”. Thus Syria + CPI = Spike.

‘Course come Thursday came the negative news. Wholesale inflation (the Producer Price Index) for November recorded a +0.4% pace, the fastest across the past seven months… Whoops! But whilst the FinMedia rather skirted the issue, not so did the Dollar, nor the Bond nor Gold, the rationale being that perhaps the Fed shan’t cut. In turn, the Dollar got the Bid, the Bond did the skid, and Gold hit the lid. PPI + Rate Doubt = Sink.

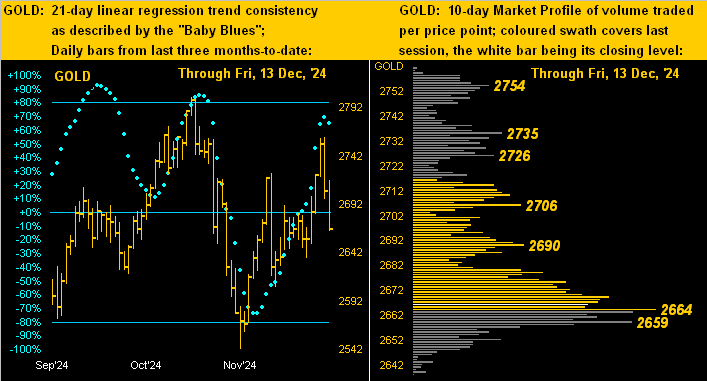

So as we go to Gold’s weekly bars from a year ago-to-date, the rightmost closing nub shows barely a net change from a week ago — despite the “spike n’ sink” — as the parabolic Short trend continues. Today at 2666, Gold sits -116 points below the ensuing week’s flip-to-Long level of 2782; thus if you’re scoring at home, given Gold’s expected weekly trading range is now 90 points, ’tis likely the Short trend shall still be in place in a week’s time: