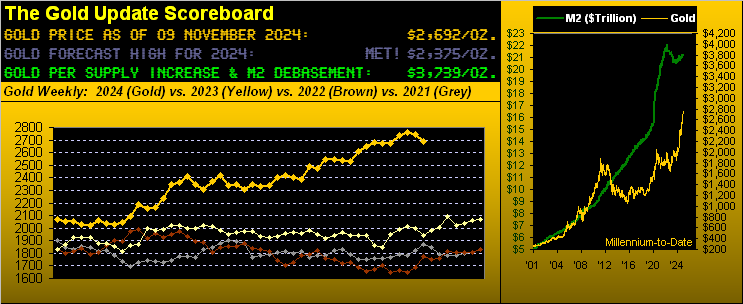

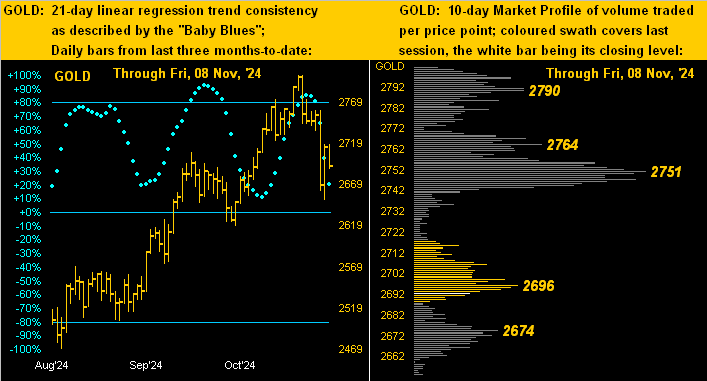

Gold’s +35.2% rally this year from 2072 to an All-Time High at 2802 might be couched catalytically as geo-political discomfort were (amongst other rationale) Vice President Harris to have defeated former President Trump, in turn installing her as the so-called “Leader of the Free World” come 20 January.

Whilst we understand significant angst is now running through the StateSide media over the election, on this Side of the Pond one senses relief being broadcast not so much that he won, but rather that she did not win, a reminder that Europe would still look to the U.S. in dire times.

Regardless, last Tuesday brought the reverse result, StateSide equities getting a sensational bid, and Gold — thus “Trumped” — was dumped.

So with respect to Gold, whenever it or any major financial market reaches levels of excessive near-term — or in the case of equities long-term — overvaluation, we provably know throughout history that it “corrects”, (or in simple jargon for you WestPalmBeachers down there, it “goes down”).

And typically, the distance back down reverts to one or more of the following: a measured mean; a targeted cluster of previous price structure; a notable prior high or low; and/or a retracement as guided by the mathematics of one Leonardo Pisano detto il Fibonacci, (aka “Signore Golden Ratio“).

‘Course, in addition to the distance of adversity, the most commonly-asked question with respect to price commencing a fall is: “When?”

Here at deMeadville, astride our many years of quantitative crunching, we like to think we’re ahead of the game in anticipating such overdue price movements — be they up from undervalued or down from overvalued — the bane of that being we’re oft just too damn early by such assessment to be timely for today’s trading community. ‘Tis why, as stated on our homepage: “…deMeadville is not for the low-information, short-attention span, instant gratification crowd…”, such lost souls otherwise permeating today’s Investing Age of Stoopid.

But in due course, quantitative analyses will out upon FinMedia dissemination of a “catalyst”, following which it all goes wrong for a spell. (Indeed, some entities — as were WorldCom, Enron, Lehman, et alia — never recover).

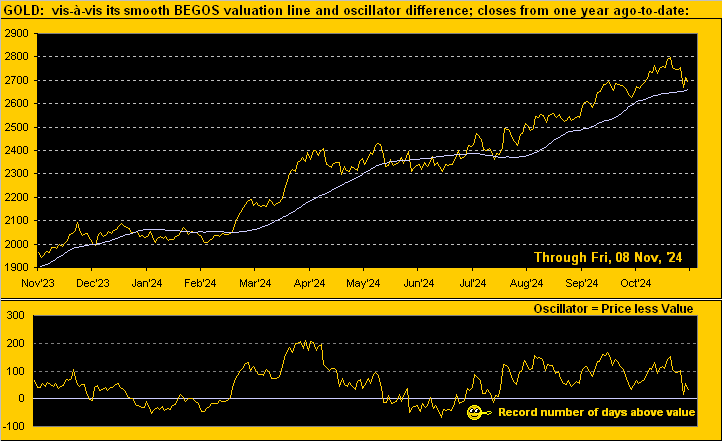

Fortunately for Gold, it always recovers and demonstrably so since President Nixon nixed the Gold Standard back in ’71. Thus when Gold swiftly dips as it just did within a six-trading-day stint — from Halloween into the StateSide election — by careening -151 points (-5.4%), ours is not to reason why. For, (albeit a bit ahead of the curve), we’ve nonetheless been anticipating such a drop. And if you read these weekly missives, you too already know — at least quantitatively — why. Cue our Market Values chart for Gold from one year ago-to-date: