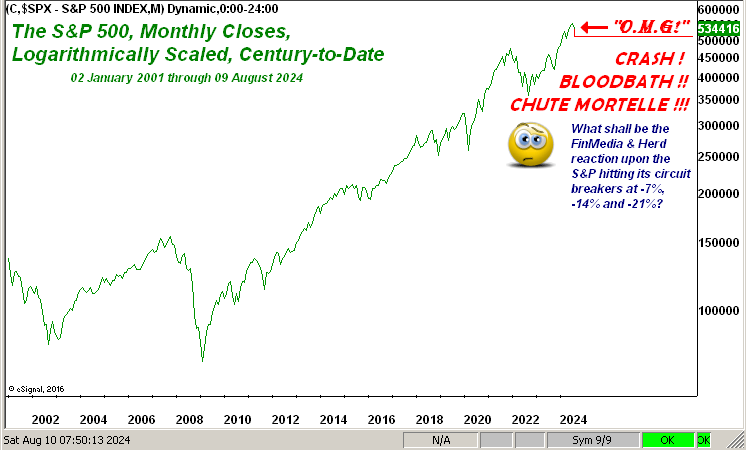

To be sure, the whole FinMedia & Herd insanity emphasizes the parroting that passes sadly for “informative news”, (which is why some three decades ago we stopped watching “CNBS”, et alia). The optics are that news entities no longer do the math; rather they just follow right along with competing agencies’ reports whist trying to outdo each other’s adjectives. Hence our presentation of the above chart. And given that correct perspective, “The Sell” obviously was nothing, and further, the S&P has come all the way back up to the “pre-disaster” level, toward settling yesterday (Friday) at 5344. But as noted in the chart, the circuit breaker “limit-down” days are coming. Ensure you’ve plenty of popcorn to enjoy that FinMedia & Herd meltdown.

As to the current state of the S&P 500:

- ‘Tis now 12 days “textbook oversold”, although just mildly so;

- With a week to run in Q2 Earnings Season, 70% of companies have bettered their year-ago bottom lines, which is an above-average pace;

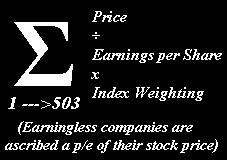

- But the Index’s albatross ’round the neck remains its exceedingly high “live” price/earnings ratio, now 38.6x — with risk-free money still paying 5% — should you care to do the math:

![]() “““Whoomp! (There It Is)”

“““Whoomp! (There It Is)”![]() –[Tag Team, ’93]).

–[Tag Team, ’93]).

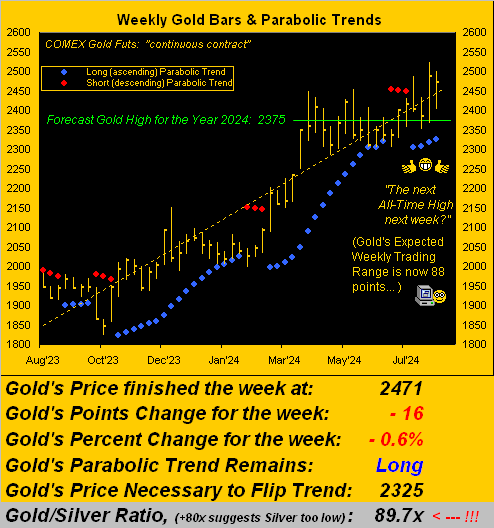

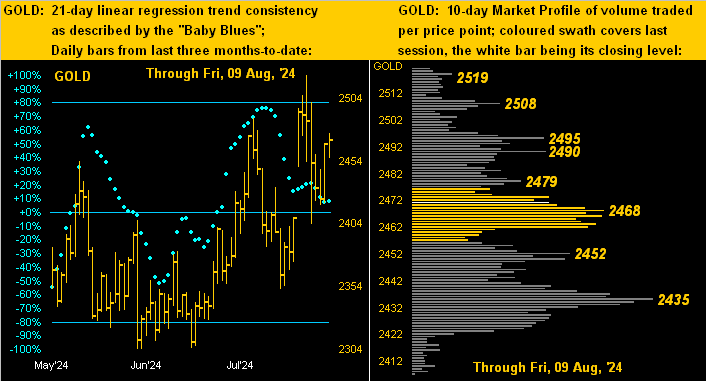

Returning to sanity, here is Gold per its chart of weekly bars and parabolic trends from one year ago-to-date. Whilst ’tis holding its area, yes, in Thursday’s (08 August) Prescient Commentary we penned: “…Gold’s daily MACD is provisionally crossing to negative: per the current Market Rhythms list, that study for the yellow metal has profited by at least $2,600/cac (regardless of signaling Long or Short) for nine of the past 10 such crossovers…” ‘Tis why we stated “provisionally”, for by Gold’s continuous futures contract, the negative MACD (moving average convergence divergence) crossover did not (at least yet) confirm. Either way, as below depicted, Gold is well within range for a fresh All-Time High (above 2538 basis December) in the new week:

‘Course, the week would not be complete without the state of the Economic Barometer, which plainly is not good.

“Dare you instead say ‘stateless’, mmb?“

Nearly so there, Squire, our having had to rescale lower the Econ Baro’s axis (which we numerically never reveal, lest the world indeed truly end). Regardless, ’tis ever so bleak. However, the Baro’s saving grace is — its mathematically being an oscillator — that it can move upward as “things get worse more slowly” (to reprise Krugman from back in ’01). And whilst this past week was very muted for incoming metrics (just five arrived), next week brings 18 reports for the Baro, which of course we update by the day per the website. Again cue the BeaTles with ![]() “““Now and Then”

“““Now and Then”![]() –[’23]).

–[’23]).

That’s right, Gools, you tell ’em, baby! To which we wrap with rates.

As you valued regular readers know, given the Baro’s blow, we’ve been knowledgeably ahead of the deteriorating curve of the economy for better than three months now. Admittedly, earlier in the year given the non-cessation of inflation, we mused over the Fed perhaps having to actually raise its rates. But the with the economy’s demise in front of our eyes, through many a recent missive we’ve stated that the Fed must cut. However, come the Open Market Committee’s Policy Statement just on 31 July, the Fed stood pat. But then the stock market made its wee crack, and all of a sudden, FinMedia & Herd are proclaiming ’tis not just that the Fed must cut, but indeed so do now as an “emergency” measure, and moreover that it be a “double cut”.

“Well, mmb, a lot has happened in the last week and a half…“

Or better stated, dear Squire, nothing recently has happened because it already had happened. ‘Tis just that the FinMedia & Herd & Fed are all behind the curve.

But don’t you get thrown a hysteria curve…

…rather with Gold maintain your verve!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro